Продукти, рішення, послуги для організацій

The year 2020 witnessed a dramatic acceleration in digital transformation, effectively moving the digital economy into the mainstream. The pandemic reminded businesses, too, of the importance of agility, further fueling the growth of digital technology across the board. In 2021, in unprecedented times, 53% of enterprises worldwide have adopted an organization-wide digital transformation strategy, representing a 42% increase compared to 2019.1 And in the Middle East, specifically, the pandemic has significantly accelerated digital transformation roadmaps — by at least one year — for 62% of organizations.2

Indeed, across the Middle East, governments have recognized that the future is digital, making it a cornerstone of national development accordingly. For example, in Saudi Arabia's Vision 2030 initiative, a Digital Economy Policy has been introduced, reflecting its significance to the country. This policy aims to have the digital economy on equal terms — as a share of total Gross Domestic Product (GDP) — with other leading global economies.3 The UAE has a similar plan, to double the size of its digital economy in just 10 years.4 Going further, the country has identified digital, technical, and scientific excellence as one of the 10 principles that will propel it into a new era of political, economic, and social development over the next 50 years.5 The UAE has also introduced sector-specific strategies to realize its vision, such as the UAE Digital Government Strategy 2025, which focuses on making the public sector data-driven and digital by design.6

Digital technologies are proliferating and touching more and more aspects of the economy, particularly in terms of the way products and services are consumed or delivered, the way transactions are conducted, and how operations are performed. It's predicted that, by 2022, more than half of the global economy will be based on, or influenced by digital.7 Naturally, these digital trends are clearly visible throughout the Middle East as well.

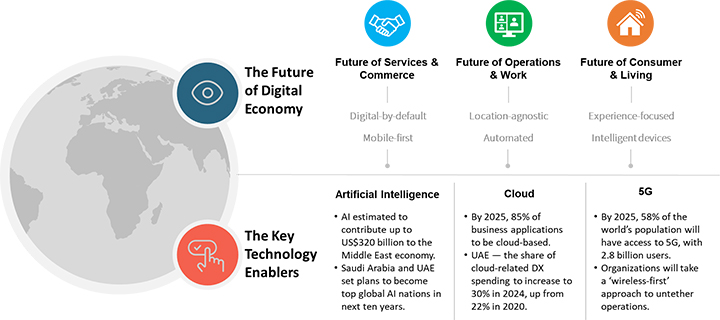

The Future of Services and Commerce: Organizations today are taking a digital-by-default approach to services and commerce. In fact, the majority of government and banking transactions today are already conducted online. The Saudi Arabian government, for example, has introduced a digital-by-default and mobile-first approach to public services as part of its Smart Government Strategy 2020–2024.8 With respect to digital commerce, the pandemic has given the already booming Gulf Cooperation Council (GCC) ecommerce sector an extra boost: it now accounts for 17% of all retail business, compared to the 3% share it enjoyed just five years ago.9

The Future of Operations and Work: Digital is also changing how work is conducted within organizations, with increasingly automated operations and location-agnostic working cultures. By 2025, it's predicted that every 10,000 employees in the manufacturing sector will be accompanied by 103 robots.10 At the same time, working culture has experienced a dramatic shift over the last two years. The hybrid work model of the future will not be constrained by the location of employees, offices, or other resources. By 2023, 70% of G2000 organizations are expected to have deployed remote or hybrid-first work models that redefine work processes.11 Furthermore, the rise of the digital economy and an improvement in digital infrastructure will bring new employment opportunities, in turn changing the skill sets that are in demand.

The Future of Consumers and Living: Just as in the workplace, digital technologies have a significant impact on home life. The number of intelligent devices in homes has increased exponentially, and this trend is expected to continue, going forward. By 2025, 20 billion smart home devices are likely to be in operation, with 14% of families worldwide having a smart domestic robot at home, and 90% of people using personal assistants on their smart devices.12 Intelligent devices also play a role in the way consumers interact with enterprises. It's estimated that, during the pandemic, customers spent 25% more time with those companies whose digital transformation plans enabled them to quickly and easily adapt to the realities of the crisis.13

As economies and enterprises move toward a digital future, certain key technologies will prove essential to their transformation journeys. Investment in these technologies — which include Artificial Intelligence (AI), the cloud, and 5G — will act as a catalyst for the growth of the digital economy.

AI: The success of a digital enterprise depends on its ability to provide superior customer, employee, and ecosystem experiences at scale. Such delivery is achieved through investment in AI. Accordingly, AI is a key area of focus in most enterprise-wide digital transformation projects and programs, and many nations across the world, including several in the Middle East, have also pledged to focus on the technology. By 2031, the UAE aims to become one of the world's leading nations in terms of AI,14 while Saudi Arabia has plans to invest US$20 billion in AI by 2030. Saudi Arabia also plans to create 300 AI startups, educate 20,000 specialists in the field, and make 40% of the national workforce data and AI literate.15 In return, over the next 10 years, AI is expected to contribute up to US$320 billion to the Middle East's economy.16

Cloud: With its distributed and as-a-service nature, cloud fundamentally democratizes access to the building blocks of innovation. The shift to cloud has therefore brought a radical change to the business landscape, with smaller organizations now having access to unlimited computing power, storage, and the most modern software available, without the need for a large, upfront investment. Taking in the wider picture, the majority of forward-thinking organizations today have a cloud-first strategy within their infrastructure as well as application modernization plans. As enterprises look to enhance their digital capabilities and intelligently use data, faster access to digital technologies built on a cloud foundation becomes imperative. By 2025, companies around the world are all expected to use cloud technology in some way, with 85% of business applications predicted to be based on it.17 In the UAE, for example, the share of cloud-related digital transformation spending is expected to increase to 30% in 2024, up from 22% in 2020.18

5G: The digital economy is made up of digital interactions between customers, employees, things, processes, and applications, with connectivity cast as the critical enabler. The pandemic further underlined the importance of connectivity as organizations focused on providing employees remote access to mission-critical systems and processes, and customer facing services shifted online. The future of connectivity revolves around facilitating the timely movement of data across people, things, applications, and processes. In this respect, 5G — with its low latency and high capacity — will prove essential to facilitating seamless digital experiences. By 2025, 58% of the world's population is expected to have access to 5G, with 6.5 million 5G base stations deployed and 2.8 billion users. GCC countries are already among the world's leaders when it comes to 5G connectivity, with early launches, fast speeds, wide coverage, and sustained investment. As a wireless-first approach becomes the norm, accelerated investment in 5G will help organizations untether their operations and evolve into digital enterprises.

The future is digital and technology will be the competitive differentiator. In this pandemic-accelerated new normal, organizations are divided into two categories: the digitally determined and the digitally distraught. Digitally-determined organizations have a holistic digital strategy for people, processes, technology, data, and governance. Accordingly, they create superior customer, employee, and ecosystem experiences. The digitally distraught, in contrast, lack enterprise-wide strategies and plans, and only make fragmented and disjointed attempts to go digital. To thrive in the new world, organizations must understand their level of digital maturity. They must also embark on journeys to become digitally determined, addressing challenges such as legacy systems, siloed technology environments, unstructured and unused data, and a lack of skills.

After 18 months of shock, the global economy is slowly recovering to pre-pandemic levels. The Organization for Economic Cooperation and Development (OECD) projects strong global GDP growth of 5.7% in 2021, and 4.5% in 2022.19 However, recovery remains uneven across economies. The nations that focus on building digital economies, supporting the digitally-determined organizations within their jurisdictions, are faring better and are, indeed, better positioned to build resiliency against future disruptions. In this regard, nations in the Middle East are on the front foot, with strategies and initiatives focused on AI, the cloud, 5G, data, and skills already in place. Enterprises in the region that have embarked on digital journeys, therefore have significant opportunities to overcome challenges through infrastructure and application modernization. However, coordinated efforts between key stakeholders — including policymakers, enterprises, technology providers, and academia — are needed to ensure digital resiliency and ongoing innovation.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy, position, products, and technologies of Huawei Technologies Co., Ltd. If you need to learn more about the products and technologies of Huawei Technologies Co., Ltd., please visit our website at e.huawei.com or contact us.

Why campuses hold the key to accelerating a net zero future

Toward Excellence in the Digital Economy

The Digital Economy: The Middle East's New Growth Frontier

Digital Economy: The Impact on National Transformation and Businesses

Accelerating the Digital Economy: Four Key Enablers

National Digital Transformation and Smarter Cities: Eight Forces That Will Shape the Future

Copyright © 2026 Huawei Technologies Co., Ltd. Усі права захищені.