This site uses cookies. By continuing to browse the site you are agreeing to our use of cookies. Read our privacy policy>

![]()

This site uses cookies. By continuing to browse the site you are agreeing to our use of cookies. Read our privacy policy>

![]()

Produits, solutions et services pour les entreprises

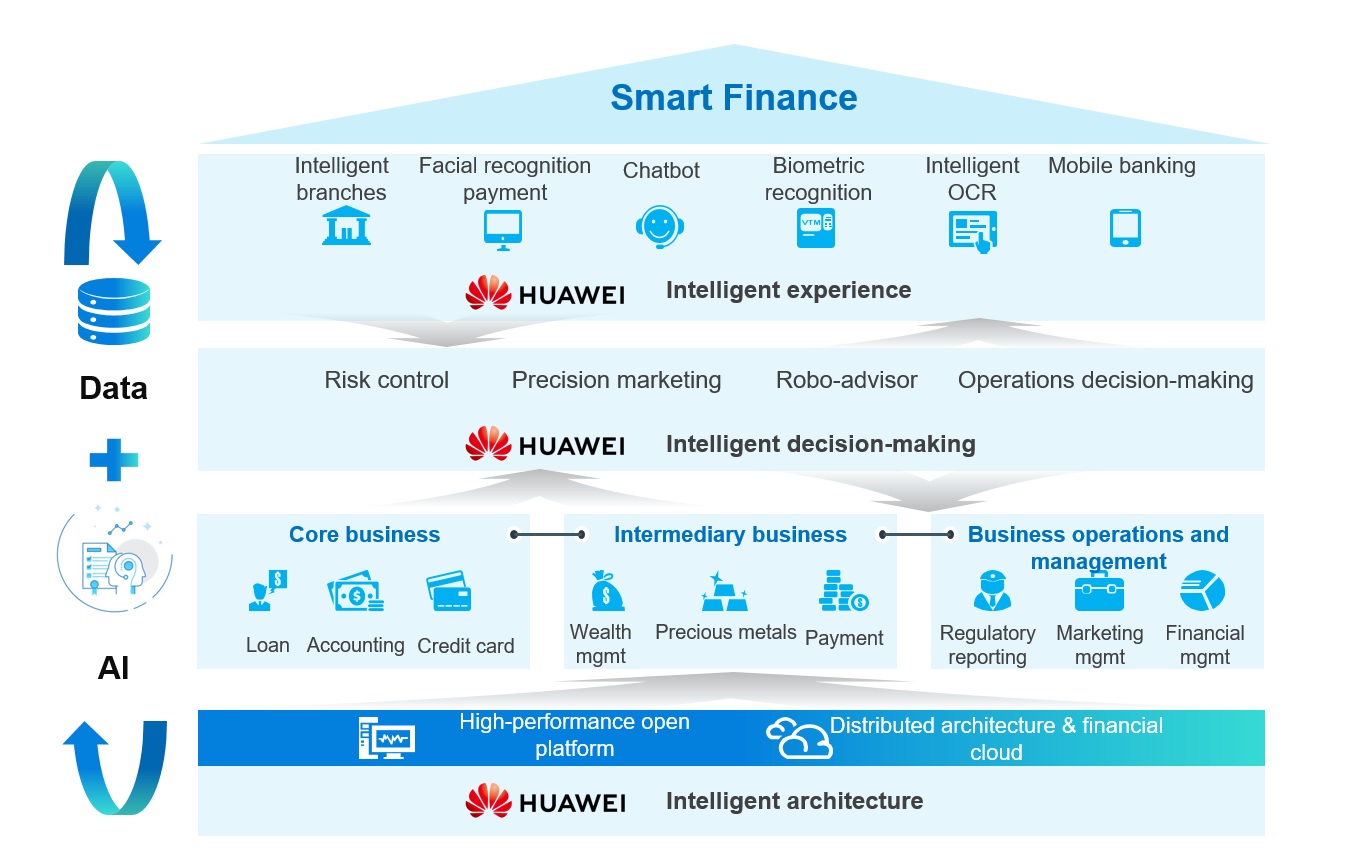

Financial institutions face a range of challenges, from intensified competition and changes in customer behavior, to stricter regulation and sluggish profit growth. To address these challenges, they are accelerating digital transformation and adopting "mobile first" and "data-driven" strategies to improve customer experience, efficiency, and risk control, all while reducing costs. These initiatives will drive business innovation, build a more open financial service platform and ecosystem, and deliver boundless intelligent financial services.

Brett King, a banking futurist, describes the financial future in his book Bank 4.0: "banking everywhere, never at a bank." Thus, the digital transformation goal of banks, as well as traditional institutions that aim to build comprehensive intelligent finance, is now to develop boundless intelligent banking services that can be embedded in multiple real life scenarios. To make this happen, the goal must be approached from three directions.

Many banks have adopted a "mobile first" strategy, not only to develop mobile digital channels, but also to transform channel services and improve the customer experience. For instance, analyzing annual reports and publicly available data of China Merchants Bank (CMB), the secrets to CMB's enhanced customer loyalty and customer experience lie in "mobile first": the bank set its "Polaris" business goal, considered Monthly Active Users (MAUs) to be its appraisal criterion, and launched two mobile apps, CMB App and CMB Life App. Combined, these efforts successfully attracted more retail banking customers and boosted their active rate, creating an edge for CMB in retail banking services. Similarly, BBVA, DBS Bank, and other international banks have gained a competitive advantage through digital transformation.

Financial institutions are embedding financial services into real life scenarios, continuously innovating their services, and making more intelligent and accurate decisions based on data. However, compared to Internet companies, which naturally have a large amount of online data at their disposal (for example, search, online shopping, and social habits), traditional financial institutions only have access to limited, traditional financial behavior data (such as financial transaction and asset information). Indeed, such traditional institutions face an even more challenging situation, with an increasing number of Financial Technology (FinTech) companies — with a background operating in the Internet — entering the financial market. To cope with this challenge, traditional financial institutions need to build an ecosystem and obtain data through service innovation or cross-industry operations, such as ICBC Link, ICBC Mail, and BOC Mobile. Meanwhile, they should also focus on obtaining offline user data (on energy consumption, goods, vehicles, and more) and fully benefit from the development and application of 5G, Internet of Things (IoT), and other technologies.

For historical reasons, the architecture of traditional financial institutions uses traditional, legacy technologies. In addition to high costs and difficult maintenance, such architecture fails to support rapid service volume growth or the fast development and deployment of new services, severely hindering overall business development and, ultimately, digital transformation. Therefore, financial institutions are in urgent need of IT architecture that uses open technologies and is distributed, to support service innovation, business agility, intelligent analysis, and business development strategies such as platform and ecosystem. Of course, while the technical architecture and the core system needs to remain stable, to continue to support traditional services, a new architecture (and core) must accommodate new services and applications that are native to cloud technologies and services. The two kinds of architecture will likely co-exist for approximately three to five years — as a "bi-modal architecture." During this period, services will gradually migrate from the traditional core to the new digital core, with load migration from mainframe or midrange computers.

To date, Huawei has served more than 1000 financial institutions around the world and established strategic partnerships with over 20 large financial institutions. The collaboration covers products, architecture, and joint solution innovation. With AI + DATA as the core, and with full-stack, open intelligent IT architecture as the foundation, Huawei helps financial institutions achieve a boundless intelligent experience, real-time intelligent decision-making, and agile, innovative, intelligent finance.

Adopting a customer-centric approach, Huawei works with partners worldwide to build open financial ecosystems. Together, we provide customers with intelligent financial solutions. Indeed, According to IDC's Global Digital Banking Readiness Index (GDBRI), China leads the way — outpacing both North America and Western Europe — in digital readiness, especially in terms of next generation digital channels, payment systems, and core banking system transformation. Based on this, Huawei, a preferred partner for financial institutions embarking on digital transformation, promotes the best practices of China's financial institutions in other regions. For example, FINCUBE is a solution developed by Huawei and a leading partner based on open and distributed technologies. The Solution helps banks construct new digital banking core systems for Bank 4.0.

In the future, we will provide a complete portfolio of mature infrastructure solutions to help customers address the challenges of openness, cost, and management efficiency in digital transformation. More importantly, we will also explore how to use open data platforms (big data + databases), AI, 5G, and IoT to develop future-oriented intelligent banking solutions, which will improve financial services and bring shared success to ecosystem partners.

Copyright © 2026 Huawei Technologies Co., Ltd. All rights reserved.