Produits, solutions et services pour les entreprises

The financial industry is entering one of the most profound transitions in its history. For more than a decade, the digital economy—powered by mobile payments and online platforms—reshaped how consumers transacted and how banks delivered services. But in 2026, a new force is taking center stage. It is faster than digital, more autonomous than mobile, and more deeply embedded in everyday life than any previous wave of innovation. We call it the Intelligent Real time Economy, and it is redefining what it means to be a modern financial institution.

In China, this shift is already visible in the most ordinary moments. A customer can order a suitcase at 1:30 in the morning and have it delivered to their doorstep within half an hour. This is not a premium service or a special promotion—it is simply how instant retail works today. Behind that seemingly simple experience lies a complex choreography of logistics, payments, credit, and risk decisions happening in milliseconds. And it is this new expectation of immediacy that is forcing financial institutions to rethink their products, their technology, and their operating models.

To support instant retail, banks are moving beyond traditional offerings and creating financial products that operate at the speed of real time commerce. Warehouses now require SKU velocity financing that adjusts automatically with inventory movement. Merchants expect atomic settlement that turns every transaction into immediate revenue. Delivery riders rely on liquidity on demand models that stream wages as they work. And consumers increasingly prefer contextual autonomy, where payments disappear into the background and transactions become invisible. These innovations are only possible when banks combine AI at scale, real time data processing, and cloud native core systems capable of handling massive data flows, instant payments, autonomous decisioning, and real time risk control.

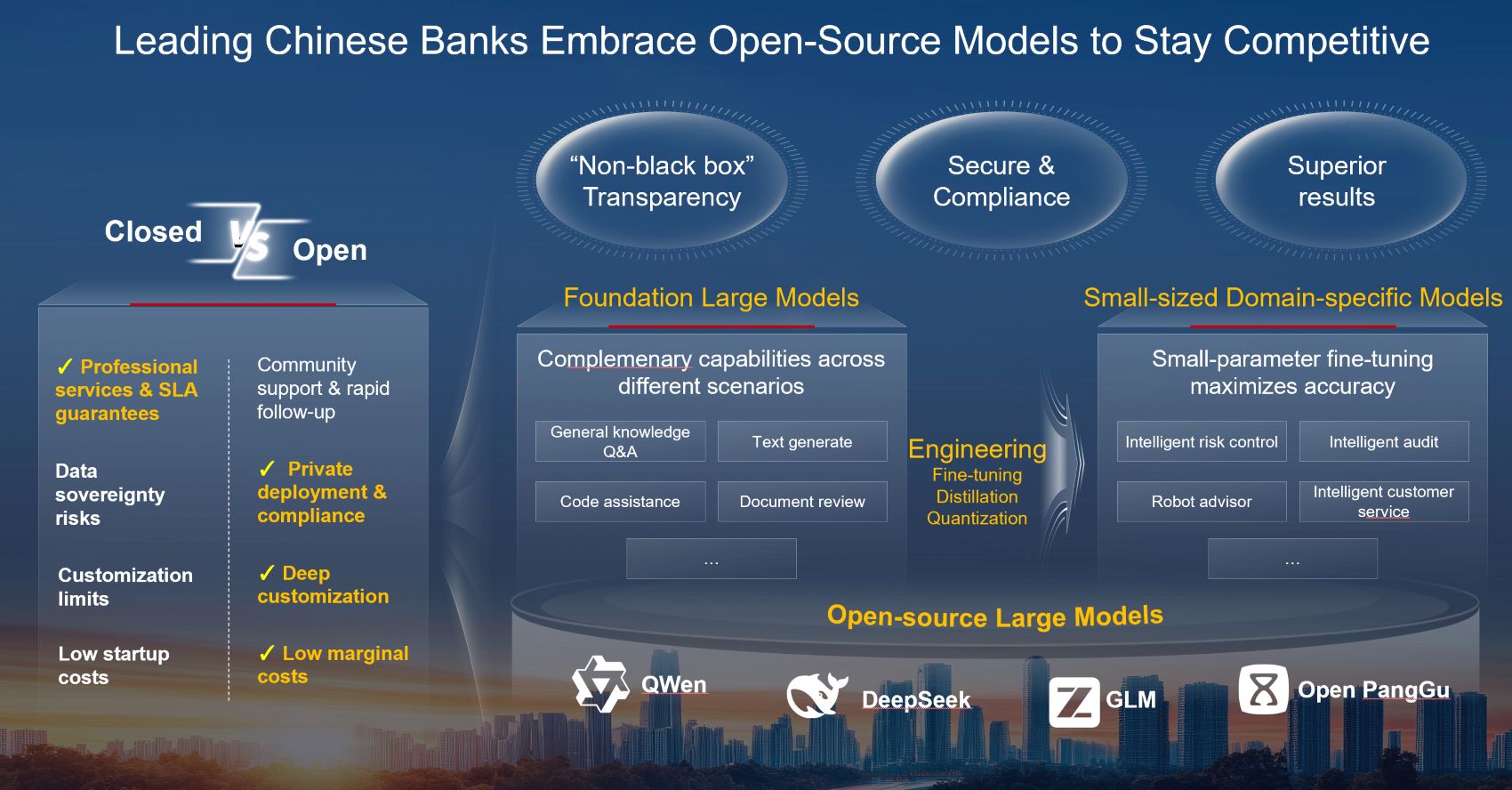

If the Intelligent Real time Economy is the new environment, then AI is the engine that powers it. Nowhere is this more evident than in the rapid rise of large language models. The debate between closed source and open source AI has become a strategic question for banks, not a technical one. Closed source models offer professional support and predictable service levels, but they come with data sovereignty concerns and limited customization. Open source models, on the other hand, provide transparency, private deployment, deep customization, and dramatically lower marginal costs—advantages that have led many of China’s leading banks to embrace them as the foundation of their AI strategy.

These banks are not simply adopting models; they are engineering them. They begin with foundation models for general intelligence, then refine them through fine tuning, distillation, and quantization to create small, domain specific models that outperform larger systems in real banking scenarios. The results are striking. One major bank built a risk analysis agent spanning nine risk domains, from financial analysis to settlement behavior. Using a foundation model alone, adoption was modest. But once the bank infused its own business knowledge and applied model engineering, adoption soared from 12 percent to 57 percent, and ultimately to 86 percent. The lesson is clear: in the age of AI, business knowledge becomes competitive advantage, and domain models become the vehicle for delivering it.

The same engineering mindset is transforming application modernization. With open source, on premise agentic coding tools such as CodeArts, banks in China have accelerated modernization projects by more than a factor of ten. What once required large teams and long timelines can now be achieved with AI driven migration engineering that preserves security, reduces cost, and dramatically increases speed.

This brings us to the third story: the “Missing Middle.” Innovation creates prototypes, but engineering creates scale. Many institutions excel at building proofs of concept, yet struggle to bring them into production across the enterprise. China’s banks have demonstrated that engineering excellence—migration engineering, performance engineering, resilience engineering, automation engineering—is the bridge that carries organizations from “0 to 1” and then from “1 to N.”

The scale of modernization achieved in China is unprecedented. National banks have migrated hundreds of millions of accounts—650 million in one case, 740 million in another—within five years. Regional banks have completed migrations of 90 to 160 million accounts in as little as two to three years. These are not incremental upgrades; they are full scale transformations that eliminate legacy systems and establish cloud native cores capable of supporting the next decade of intelligent, real time financial services.

Taken together, these three stories reveal a clear trajectory for the future of banking. The industry is moving beyond digital channels and into a world where intelligence, autonomy, and real time responsiveness define competitive advantage. Banks that embrace open source AI, engineer domain specific intelligence, and modernize their core systems at scale will be the ones that lead in the Intelligent Real time Economy.

The journey beyond digital has already begun, and the institutions that act now will shape the next era of global finance.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy, position, products, and technologies of Huawei Technologies Co., Ltd. If you need to learn more about the products and technologies of Huawei Technologies Co., Ltd., please visit our website at e.huawei.com or contact us.

How GenAI Sparks Growth and Innovation in Leading Banks

4 Zeros Resilience Underpins the Path to AI Banking

Boost Resilience, Reshaping Smarter Finance Together

Non-Stop Banking, Resilience Boosts Intelligence

Navigate Change, Shaping Smarter Finance Together

Accelerate Change, Shaping Smarter Greener Finance Together

3 Ways Huawei Is Unleashing the Value of Digital for Finance

Copyright © 2026 Huawei Technologies Co., Ltd. All rights reserved.