Productos, soluciones and servicios para los negocios

Banking’s next transformation is not about channels, apps or interfaces. The bank of the future may be the one we never see. The invisible bank is coming.

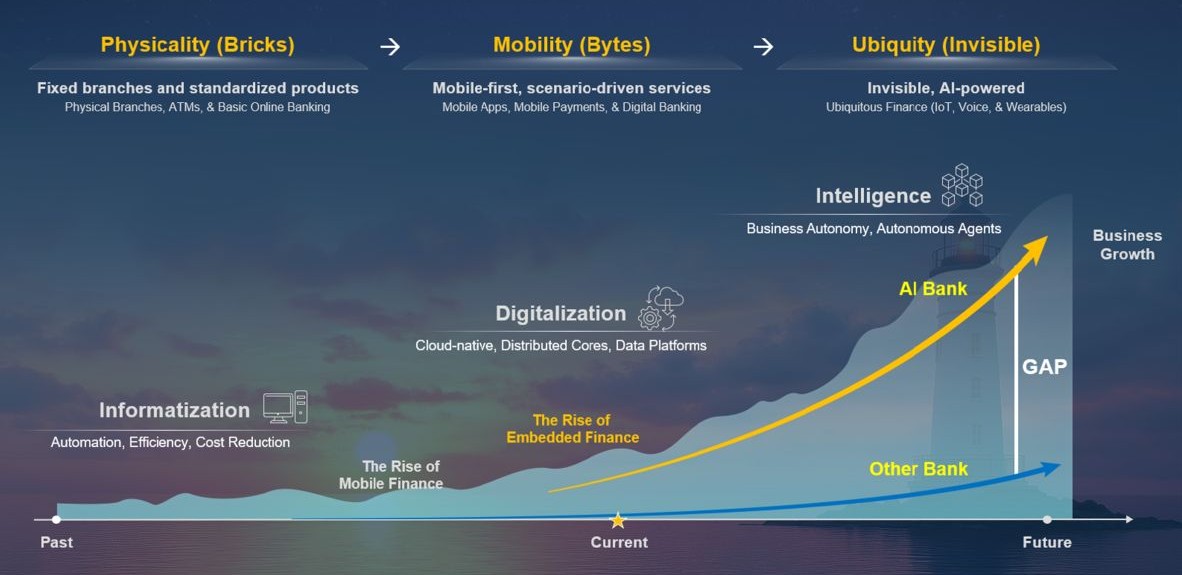

The shift has been unfolding via 3 distinct phases:

Phase 1: Branches – Banking was tied to location. You went to a branch. Products were standardized. The bank was a place you visited.

Phase 2: Mobile – Banking moved to the phone. Apps replaced branches, but customers still had to log in, search, and interact with the bank directly.

Phase 3: Invisible – Now banking is moving into the background. Services are triggered by context, decisions are increasingly supported by AI, and instead of customers going to their bank, the bank goes to them.

The evolution to the invisible bank

5 main transformation blocks are driving the shift:

1. Interactions shifting from apps and interfaces to natural language conversations.

2. Personalisation moving from a premium service to a mass capability.

3. Work increasingly organised around hybrid human–AI teams.

4. Decision making shifting from static, rule-based processes to intelligent systems.

5. Banking systems being rebuilt as AI-native architectures.

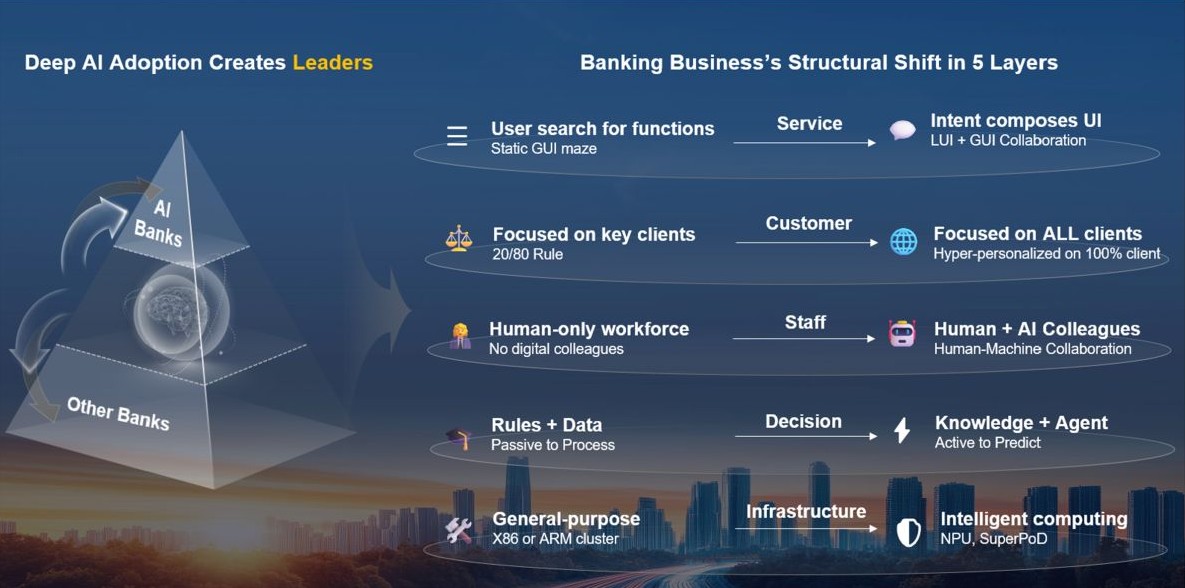

Banking's structural shift

In the future, there will be two types of institutions: those built around AI - and those merely using it.

The difference will determine who manages the transition and who struggles.

At the center of this shift lies a fundamental question:

Will AI sit on top of the bank as another layer?

OR

Will the bank itself be rebuilt around intelligence?

If the latter is true, then the real question is practical: how do banks can make that happen?

Huawei has one of the clearest transformation blueprints in the industry. They call it Intelligent Finance Value Implementer and is built around 3 pillars:

1. Scenarios:

AI starts with where the bank needs results and delivers value across 3 areas:

• Customer experience: interactions handled through conversational interfaces

• Risk & control: credit assessments, fraud monitoring, compliance checks via automated analysis

• Internal efficiency: operational workflows supported by AI assistants

2. System Engineering:

Many AI projects fail because they remain isolated pilots that never scale.

System engineering means building AI properly into the bank’s systems from the beginning - connecting data, security, governance, and infrastructure.

3. Infrastructure:

AI changes the technical demands on banking systems.

Banks need architectures combining general computing, AI computing, storage, and networking into a unified stack supporting both traditional workloads and AI-driven operations.

As AI becomes embedded across processes, systems must process data instantly, handle heavy model workloads, and remain continuously available.

If financial decisions increasingly originate from AI agents rather than humans navigating apps, banks will need to structure their products so agents can find, understand, and compare them. That means exposing financial services in machine-readable formats so AI systems can evaluate and trigger them automatically.

This means that in practice banks will have to add new layers on top of today’s infrastructure: structured product metadata, real-time decisioning endpoints (for credit, payments, FX, liquidity, etc.), and machine-readable policies and constraints.

The future bank will not only be AI-enabled internally but it will need to make its capabilities externally discoverable and usable (by AI systems).

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy, position, products, and technologies of Huawei Technologies Co., Ltd. If you need to learn more about the products and technologies of Huawei Technologies Co., Ltd., please visit our website at e.huawei.com or contact us.

Copyright © 2026 Huawei Technologies Co., Ltd. Todos los derechos reservados.